Table of Content

To maximize coverage for your home-based business, you’ll need separate home business insurance. If one of your employees gets injured or sick due to a work occurrence, workers compensation insurance pays medical bills. Sole proprietors are often exempt from workers comp requirements, but if you have employees make sure you understand your state’s workers comp laws.

If you take out a commercial loan to finance your home-based enterprise, your lender may also enforce other insurance requirements, such as general liability and professional liability insurance. Home-based business insurance may be required if you employ workers or if you have an outstanding commercial loan. Additional types of insurance policies may be necessary depending on what services or products your business offers.

How Much Does At-Home Businesses Insurance Cost?

While you shouldn't aim to be negligent, insurance will help put your mind at ease. Bodily injury coverage protects you if someone sustains an injury on your property. Personal injury refers to any injury of someone's body, emotions, or mind. If something happens to a client while at your business, you will have coverage. Then, you won't have to pay as much in damages, and you can keep your business going if something happens to your home. Dick Lavey, president of The Hanover Agency Markets, says he recommends home-based business insurance even for the simplest business pursuits.

First, you should choose a company that offers all of the coverage you need. While choosing to enroll in home-based business insurance can be daunting, know that the small monthly payment is protecting you financially in the long run. If you’re looking for additional support in getting your business off the ground, consider opening an account with NorthOne. If you’re looking for small business banking experts, visit us online and contact us with any questions you have. Discuss your business thoroughly with your insurance agent to get expert insight into all the areas in which your business may be vulnerable to legal action and get the protection you need.

Saving Money on Home Based Business Insurance

Furthermore, endorsements and riders on homeowners' policies in addition to specialty home and office policies are important coverages that small business owners should consider. In general, however, a home business insurance policy can range from $250 to $1,500 per year, depending on your needs. The majority of home-based business owners find that a business owner’s policy is the most cost-effective solution to cover both business assets and liability. BOPs are inclusive policies often starting around $250 annually, and they protect business owners from general liability incidents, business property losses, and business interruption claims. An insurance agent will be able to help you decide which choice is the best for your specific business needs.

Or maybe you teach music lessons and want to allow family members to sit in. Another type of visitor you should consider when obtaining insurance are delivery people. You may have frequent visits from a delivery driver if you order supplies online regularly. Filing a claim shouldn't affect your business's finances significantly, so keep that in mind when laying out your budget.

The Benefits of an Independent Insurance Agent

If you have employees that work from your home, you want to protect yourself against claims from them. When looking at small home-based business insurance, defining home-based businesses is essential. A home-based business is any company that operates out of your personal place of living. Even if you primarily work online, it can help to have home-based business insurance coverage. Then, if something happens to you or your home, you'll still be able to run your business. Like all businesses, home-based companies must comply with state workers' compensation laws.

Home-based businesses require some type of home business insurance. How much you need, and what type you need, depends on what type of business you run. If you have at least one employee, you may be able to buy your own group insurance plan, which could cover you and your employees. Had a great experience with Insurdinary and with Dornaz who was super helpful in finding me the best plan and the best coverage for my needs.

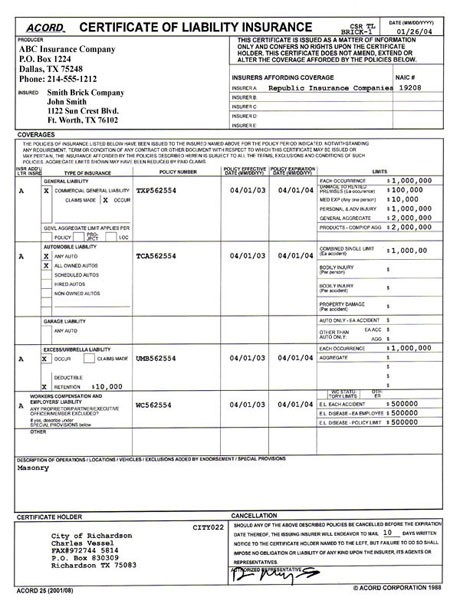

I would highly recommend her to anyone needing this kind of insurance. Dornaz contacted me regarding health, dental and drug coverage and she advised me of the costs involved for proper coverage. She also offered travel insurance but was a month too late so I will consider it late next year. You should also consider how much insurance will cost based on your business and the coverage. It's also important to know when and how you can contact the insurance company with general questions or to file a claim. Whether you provide a service, product, or both, your home may be your workplace.

Many in-home business owners and freelancers don’t realize that relying on homeowners insurance to cover work equipment can leave them with a sizable coverage gap. You can get better home-based business insurance from either an endorsement to your homeowners insurance policy or as a separate business insurance policy. In this case, Jane should purchase home-based business insurance to protect her business equipment, employees and income.

Homeowners insurance provides financial protection for your home and personal belongings if they’re damaged or burglarized, and it may cover your liability expenses if you’re sued because of an accident. However, a basic policy has limited coverage for home-based businesses. A standard home insurance policy covers only up to $2,500 of business property. So if you lose more than that in a house fire, for example, your reimbursement is limited to $2,500.

Instead, it’s a collection of policies that businesses operating out of homes usually need. Today’s digital workforce has changed not just the way employees get their work done, but where they get it done. Instead of trekking to the office each day, successful entrepreneurs and small business owners are able to operate their businesses from the comfort of their homes.

And as such, it needs to be insured just like any other brick and mortar operation. If you have any employees most states will require you to carry worker's compensation and unemployment insurance. Some states require you to insure yourself even if you are the only employee working in the business. Insurance is so important to proper business function that both federal governments and state governments require companies to carry certain types.

However, having home-based business insurance that protects you and your customers can offer you some peace of mind. Home-based business insurance is also useful if you will have a delivery person visit you often. The right policy may protect you if a delivery person trips or experiences another injury on your property. Home-based business insurance is a type of insurance that protects you and your business if you work from home. The most obvious use for this is if your business brings clients to you. If you’re running a business out of your home, having the right insurance coverage to protect your assets over the long term is essential.

Every business can benefit from insurance, and the right coverage will protect the owner and any employees from potential liabilities. This would be good for a very small business with annual sales around $5,000 or under. The Small Business Health Options Program, or SHOP, is a government-run health insurance program designed to help small businesses.

Comprehensive or all-risks insurance isn’t enough because it covers you for dangers to your home structure, not your business operating within it. These days, many successful entrepreneurs and small business owners operate their businesses from the comfort of their homes. But just because you can run your business wearing fuzzy slippers doesn't mean that it's not a real business.

No comments:

Post a Comment